Drug Channels delivers timely analysis and provocative opinions from Adam J. Fein, Ph.D., the country's foremost expert on pharmaceutical economics and the drug distribution system. Drug Channels reaches an engaged, loyal and growing audience of more than 100,000 subscribers and followers. Learn more...

Today’s guest post comes from William Grambley, Chief Product Officer at AssistRx.

William discusses four specific uses cases for how AI can create efficiencies and improve patient support programs for both healthcare providers and patients. He provides three considerations that life sciences organizations should evaluate when adopting AI in their patient support programs.

Drug Channels Institute’s (DCI’s) latest analysis reveals that PBM-affiliated specialty pharmacies continue to dominate the dispensing of specialty drugs.

DCI has identified nearly 1,900 dispensing locations with specialty pharmacy accreditation. Below, we share DCI’s latest analysis of the top 15 specialty pharmacies, including updated market shares and revenue estimates.

As in prior years, pharmacies linked to the three largest pharmacy benefit managers (PBMs) accounted for two-thirds of prescription revenues from pharmacy-dispensed specialty drugs. We also explore how these pharmacies contribute to PBMs’ profitability—and spotlight the growing influence of provider- and health system-owned dispensing channels.

Once again, “specialty” mostly means affiliated with a PBM.

In today’s fast-moving pharmaceutical marketplace, insight is everything. Whether you're building trust with customers, launching new products, or guiding internal teams, understanding the economic forces that shape drug distribution, reimbursement, and pricing is essential.

At Drug Channels Institute (DCI), we know how critical this knowledge is—and how hard it can be to find credible, up-to-date training that fits into a busy professional’s schedule. That’s why we created our DCI eLearning Modules: a suite of six interactive, expertly narrated courses that deliver must-know insights in 45 minutes or less.

These modules were built from the ground up for pharmaceutical professionals—from seasoned experts to newcomers looking to understand the industry's complex web of relationships. Each course distills our signature Drug Channels expertise into engaging, bite-sized lessons that are ideal for:

Sales and field teams: seeking clearer context for their customer conversations

Market access, training, and internal strategy groups: who need to understand payer and channel dynamics

Any professional: ready to level up their understanding of pharmaceutical economics

Each module features:

Interactive graphics and animations for improved retention

Expert voice-over narration to guide you through complex topics

References to key DCI reports for optional deep dives

iPad compatibility for learning on the go

The modules are available only via a site-wide license, giving your entire organization access through your internal learning platform. We also offer licenses to our secure hosted learning environment—no internal setup required! (Sorry, individual licenses are not currently available.)

What You’ll Learn: A Snapshot of Each Module

1. Follow the Dollar: How Funds Flow in the Distribution and Reimbursement Channels

This foundational course breaks down the financial and product flows in U.S. pharmaceutical distribution. You'll learn how money and medicines move between manufacturers, wholesalers, pharmacies, PBMs, and payers—and how each relationship affects costs and outcomes.

2. The Economics of Retail, Mail, and Specialty Pharmacies

Gain a clear-eyed view of how different pharmacy channels generate revenue and manage costs. Understand reimbursement dynamics, cost estimation methods, and how profitability varies across drug types and dispensing models.

3. The Business of Specialty Pharmacy

Specialty drugs are revolutionizing care—and reshaping the pharmacy business. This module explores how these products are distributed, covered by insurance, and supported through value-added services.

4. The Economics of Provider-Administered Specialty Drugs

Navigate the unique dynamics of provider-administered drugs, from buy-and-bill systems to ASP reimbursement. Understand how coverage types, care sites, and financial relationships affect access and profitability.

5. Understanding Pharmacy Benefit Managers

PBMs wield enormous influence—but many professionals may not fully understand their true impact. Learn how PBMs operate, where they make money, and how they interact with manufacturers, payers, and pharmacies.

6. Pharmaceutical Wholesalers: Business Strategies and Financial Economics

Take a deep dive into how wholesalers operate, generate profits, and provide critical services. You’ll come away understanding the difference between full-line wholesalers and specialty distributors—and why that matters for your strategy.

Bottom line: If you or your team work in any part of the pharmaceutical value chain, DCI’s eLearning modules will make you smarter, faster. They’re the shortest path to mastering the industry's most important (and most misunderstood) topics.

Today’s guest post comes from Jim Hundemer, Chief Information Security Officer (CISO), and Sudhakar Velamoor, Chief Technology Officer (CTO), of Kalderos.

Jim and Sudhakar discuss some of the complex challenges manufacturers face as they deal with outdated data systems, information silos, misapplied discounts, and growing cyber security threats. They argue that these challenges will lead to lost revenue, third-party security breaches, and diminished patient care.

It's time for Drug Channels’ annual update of vertical integration among insurers, PBMs, specialty pharmacies, and healthcare services within U.S. drug channels. As you can see below, we have revised, renovated, and refurbished our infamous illustration of the major vertical business relationships among the largest companies.

Proponents of these vertical integration arrangements argue that they create opportunities to mine healthcare costs. However, these organizations remain highly controversial, due to the potential for anti-competitive behavior. We summarize some of the key issues below.

While some major companies have narrowed their focus or unwound previous integration efforts, ongoing consolidation and selective deconsolidation will continue to reshape the healthcare biome by trying to build something epic, block by block.

It's time for Drug Channels’ annual examination of U.S. brand-name drug pricing.

For 2024, average brand-name drugs’ list prices grew by only 2.3%. What’s more, after adjusting for overall inflation, brand-name drug net prices dropped for an unprecedented seventh consecutive year. Details and additional commentary below.

As I predicted two years ago, the combined impact of changes to Medicaid rebates, the Inflation Reduction Act (IRA), and novel formulary access strategies have led multiple manufacturers to pop the gross-to-net bubble for high-list/high-rebate products. Consider the 18 products with list-price cuts shown below. Other drugmakers have reduced the rate of price increases, thereby inflating the bubble more slowly.

Employers, health plans, and pharmacy benefit managers (PBMs) determine the extent to which patients with insurance share in this ongoing deflation. But signs of change to the conventional approaches are undeniable.

New channel models—including smaller PBMs, cost-plus pharmacies, patient-paid discount card prescriptions, and manufacturers’ direct-to-patient businesses—are creating novel paths for drugs that can be sold without gross-to-net bubble distortions.

The bubble won’t vanish overnight. But for the first time in years, I can foresee a time when SpongeBob SquarePants will move on from Drug Channels.

ICYMI, the largest three pharmaceutical wholesalers—Cardinal Health, Cencora, and McKesson—are using vertical integration to build significant market positions in businesses beyond drug distribution.

In the video clip below, I review the vertical integration status of the largest three pharmaceutical wholesalers, illustrated in the chart below.

[Click to Enlarge]

I also:

Explain how wholesalers have strengthened their position in buy-and-bill channels for provider-administered drugs through vertical integration with their downstream customers.

Discuss how and why private equity roll-up activity has provided wholesalers with strategic opportunities to acquire ownership stakes in practice management companies.

Outline the market access implications for provider-administered biosimilars in the buy-and-bill market.

It’s time to pay attention to the money behind the 340B curtain.

Minnesota just released the industry‘s first ever mandated financial report on the 340B Drug Pricing Program. Below, I do a wicked deep dive into the data and highlight crucial implications about spending, profits, pharmacies, plans, patients, program integrity, and more.

There are important limitations to these data. But Minnesota’s report marks a valuable first step on the yellow brick road to the wonderful world of transparency. I suspect similar reports are gonna be popular.

For 2025, the three largest pharmacy benefit managers (PBMs)—Caremark (CVS Health), Express Scripts (Cigna), and Optum Rx (United Health Group)—have again each excluded hundreds of drugs from their standard formularies. You can find our updated counting below.

As you’ll see below, the combination of formulary exclusion and private labels is creating an increasingly confusing and crowded biosimilar marketplace.

For 2025, the Big Three PBMs shifted national formularies to favor their private-label biosimilars over Humira and its many biosimilar competitors. In fact, nearly all marketed Humira biosimilars are excluded from the larger PBMs’ 2025 formularies. Meanwhile, Stelara—this year’s big pharmacy benefit biosimilar launch—remains on the PBMs’ formularies, but will share space with PBMs’ private label products.

Like it or not, PBMs’ financial benefits from their private-label product align with the benefits to plan sponsors and patients. But the PBMs’ strategies, combined with the warped incentives baked into the Inflation Reduction Act, raise questions about the viability of the biosimilar marketplace.

Three’s still company in the world of pharmacy benefit managers.

For 2024, nearly 80% of all equivalent prescription claims were processed by three familiar companies: the CVS Caremark business of CVS Health, the Express Scripts business of Cigna, and the Optum Rx business of UnitedHealth Group. The names haven’t changed, but shifting relationships and contract shakeups have altered the plot, with Express Scripts stepping into a new lead role.

Below, we break down the latest market share data from Drug Channels Institute (DCI), explore the developments driving these changes, and examine what they signal for the future of the PBM landscape.

Today’s guest post comes from Josh Marsh, Vice President and General Manager, Sonexus™ Access and Patient Support at Cardinal Health.

Josh discusses how patient support programs are evolving, including the shift toward outsourcing individualized hub functions. He lists five characteristics pharmaceutical companies should look for when evaluating outsourced support for long-term program success.

Spring has officially arrived in sunny downtown Philadelphia—the proud home base of Drug Channels. As you can see on the right, we celebrated in Miami at the Drug Channels Leadership Forum.

The vernal equinox also brought a surprising surge of industry updates and noteworthy news you won’t want to miss:

Blue Shield of California provides a puzzling update to its PBM unbundling effort

The Stelara biosimilar price war begins

My reaction to Optum Rx’s pharmacy reimbursement announcement

A valuable Follow the Dollar primer

Plus, Dr. Glaucomflecken reviews UnitedHealth Group's vertical integration strategy.

Paula and I are beyond grateful to everyone who took the stage to share their insights and to all who participated in making this event so impactful. (Even Paula got on the main stage!) The event was packed with thought-provoking discussions, candid insights, and dynamic exchanges. The HMP Global team delivered a truly first-class experience for the nearly 350 lucky attendees.

You can find attendees’ photos by searching “#DCLF2025” on LinkedIn. (Be sure to use quotation marks and then sort by “Latest.”)

BTW, you won’t see any news stories about the DCLF. That’s because the media were not invited and the sessions were not recorded. You had to be in the room where it happened.😉

The DCLF will return in March 2026.

P.S. A special shoutout to the phenomenal HMP Global team. Your hard work and dedication made this event unforgettable!

Pricing & Contracting USA arrives at an important moment for our industry. As you work to navigate the evolving healthcare landscape, this annual event brings together 60+ expert speakers from 70+ companies to lead the critical discussions that will drive comprehensive market strategy, uniting Medicaid, Policy, Pricing, Contracting & Reporting thought leaders.

With 52 sessions across 6 workshops and 5 tracks, this event features:

Wholesaler/Manufacturer Team-to-Team Meet-and-Greets: Direct industry collaboration

Executive Programming: Fireside Chat with External Counsel, Closed Door Executive Strategy Summit and Luncheon

Interactive Sessions: Speed Networking, AI Lunch and Learn

Strategic Working Groups: Medicaid Working Group Report, 80 Minute Industry Strategy Working Group

The Hottest Topics: Covering Government pricing, contracting and reporting fundamentals, MDRP, the Medicaid Final Rule, State Drug Price Transparency, PDAB, Medicaid, VA and IRA penalties, PBM evolution and regulation, 340B challenges, GTN, PhRMA, GPO Management, specialty distribution and cold chain, AI and automation and more.

Featuring confirmed speakers from: Pfizer, AstraZeneca, Novo Nordisk, Sanofi, Gilead Sciences, McKesson, Regeneron, UCB, PhRMA, CSL Behring, OIG, United Therapeutics, Alkermes, Averitas Pharma and many more.

Join us where Medicaid, Commercial & Government Teams will collaborate to drive a successful market strategy!

View the agenda for Pricing & Contracting USA to see the complete picture – the program, speakers, and more, and visit www.informaconnect.com/pricing-contracting-usa for further details and to register. Drug Channels readers will save 10% off when they use code 25DRCH10 and register prior to April 30, 2025.*

*Cannot be combined with other offers or used towards a current registration. Cannot be combined with special category rates or other offers. Other restrictions may apply.

The content of Sponsored Posts does not necessarily reflect the views of HMP Omnimedia, LLC, Drug Channels Institute, its parent company, or any of its employees. To find out how you can publish an event post on Drug Channels, please contact Paula Fein(paula@DrugChannels.net).

Today’s guest post comes from Greg Skalicky, President of EVERSANA.

Greg discusses some of the challenges manufacturers face with product commercialization, patient access and adherence, and negotiating partnerships with pharmacy benefit managers (PBMs). He introduces us to EVERSANA DIRECT Commercialization™, a direct-to-patient change/model.

Order before March 31, 2025 to receive special discounted pricing!

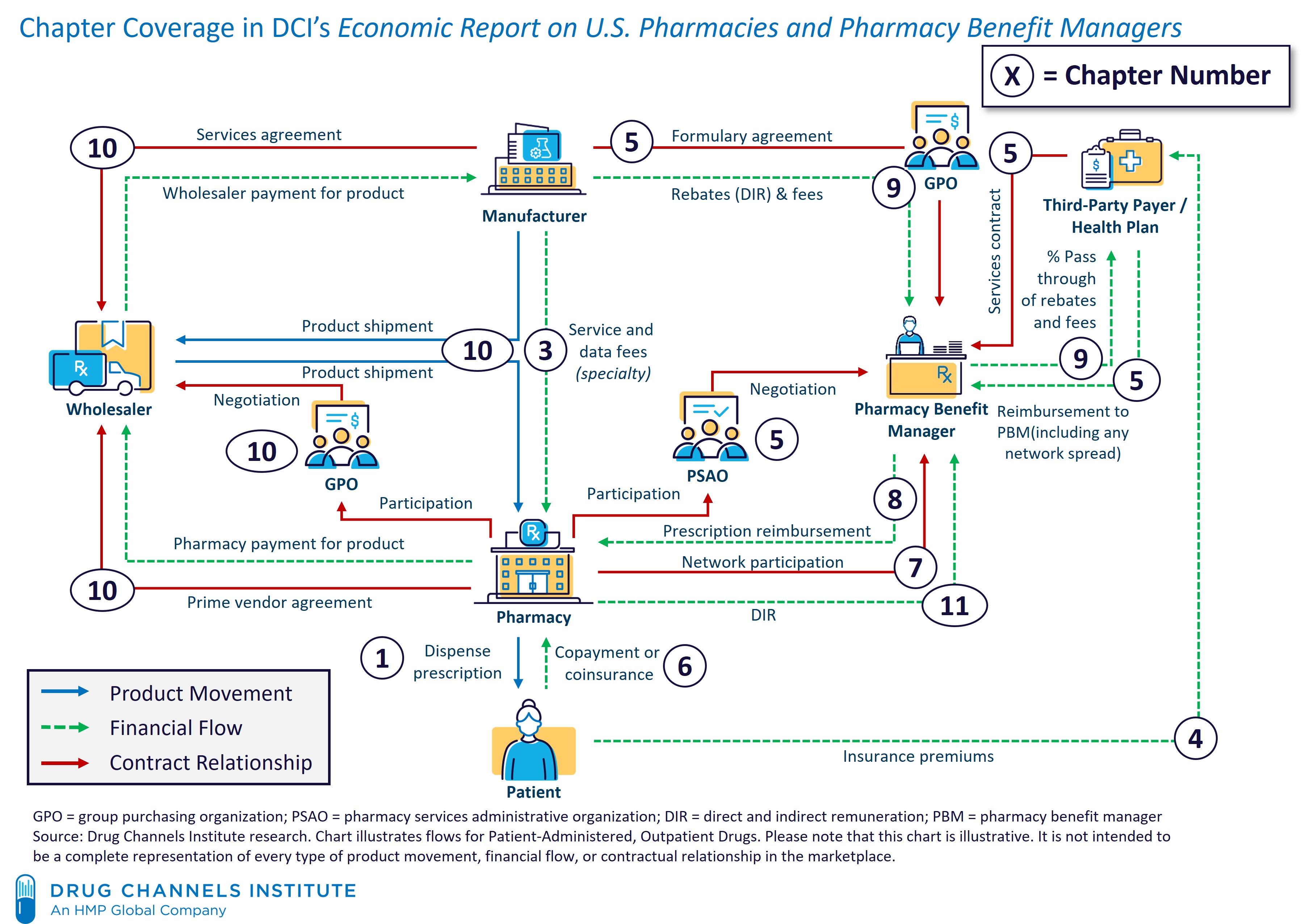

Now in its 16th edition, this report remains the most comprehensive, fact-based resource for understanding the entire U.S. drug pricing, reimbursement, and dispensing system. It serves as the ultimate guide to the complex web of interactions within U.S. prescription drug channels.

What's inside?

12 chapters, 540+ pages, and 268 exhibits

Nearly 1,200 endnotes with hyperlinks to source materials

You can pay online using Visa, MasterCard, American Express, Discover, and PayPal. If you prefer to pay by corporate check or ACH, click here to request an invoice.

Our reports are widely used by nearly every company involved in the drug channel:

Pharmaceutical manufacturers

Wholesalers, pharmacists, pharmacy owners

Hospitals, benefit managers, and managed care executives

Policy analysts, investors, consultants, and more

So, this report helps you understand what your customers, partners, and competitors are reading.

The chart below illustrates the depth and breadth of the 2025 edition, with chapter numbers corresponding to each channel flow.

FUN FACTS ABOUT THE 2025 EDITION

The 12 chapters are self-contained—you don't need to read them in order. (Really!)

There are tons of internal hyperlinks to help you navigate and focus on what matters most to you.

We’ve updated all market and industry data with the most current insights, including our annual analyses of the largest pharmacies, specialty pharmacies, and PBMs.

You have the option to download an additional PowerPoint file with images of all 268 exhibits—making it easier to share insights with your team. (Note: All license versions include exhibits within the text.)

There are a staggering 1,163 endnotes (!), most of which have direct hyperlinks to original source materials, giving you a deeper knowledge base beyond what’s in the report.

Sadly, I had to remove all corny jokes and pop culture references. So, no memes and absolutely no references to SpongeBob SquarePants.

If you have any questions (before or after reading the report), just email me.

Today’s guest post comes from Jordan Armstrong, Vice President of Business Development at AssistRx.

Jordan discusses the uptick in direct-to-consumer (DTC) models for life sciences organizations looking to navigate market challenges and improve patient access. He goes on to describe some potential risks and complexities associated with these models.

To learn about AssistRx’s technology solutions designed to simplify the patient experience and reduce channel costs, meet with AssistRx at the Drug Channels Leadership Forum, Informa Connect’s Access USA, and/or the Asembia Summit.

For 2024, DCI estimates that total prescription dispensing revenues at retail, mail, long-term care, and specialty pharmacies reached $683 billion, up 9% from the 2023 figure. GLP-1 agonist drugs remained the most significant driver of prescription revenue at retail pharmacies, accounting for more than 80% of dispensing revenue growth for 2024.

The table below—one of 268 in our new report—cues up DCI's first look at the 15 largest organizations that battled for those revenues. For a sneak peek at the complete report, click here to download our free 30-page report overview (including key industry trends, What's New in this edition, the Table of Contents, and a List of Exhibits). We’re offering special discounted pricing if you order before March 31, 2025.

Today’s guest post is from Divya Iyer, SVP Go-to-Market (GTM) Strategy at GoodRx.

Divya argues that patient support programs (PSPs) struggle with awareness and accessibility, preventing patients from fully benefiting from the financial and educational resources available to them. Divya discusses how integrating digital solutions from GoodRx can enhance engagement, streamline access to therapy, and improve patient outcomes.

Last week, President Trump signed yet another executive order, this time promising to make healthcare pricing more transparent.

While this marks another federal push for disclosure, states have already been quite active in this space. Since 2017, 24 states have passed 38 laws targeting healthcare transparency, with a strong focus on unraveling the complex economics of pharmacy benefit managers (PBMs).

But has all this legislation actually provided clarity—or just more red tape?

Below, I analyze four state reports on manufacturers’ rebate and fee payments to PBMs. The findings are dispiriting: mandated disclosures have yielded little actionable, reliable data. Lawmakers got to pat themselves on the back for “transparency,” but the data tell a different story. Federal efforts haven’t been much better.

Dr. Adam J. Fein, president of Drug Channels Institute (DCI) and the author of Drug Channels, invites you to join him for DCI’s new live video webinar:

This page describes the event and explains how to purchase a registration. The webinar will be broadcast from the Drug Channels studio in beautiful downtown Philadelphia.

Join industry expert Adam J. Fein, Ph.D., for an exclusive deep dive into the latest trends, data, and strategies shaping the pharmacy benefit management (PBM) industry. Drawing from the brand-new 2025 Economic Report on U.S. Pharmacies and Pharmacy Benefit Managers, Dr. Fein will provide invaluable insights to help you and your team stay informed about this rapidly evolving market.

Dr. Fein will share his expert analysis on critical industry developments, including:

The competitive landscape of major PBMs, with exclusive market share data from DCI

Key business trends among leading PBMs and their impact on the market

PBMs’ expanding role in specialty pharmacy and how it’s reshaping the industry

Exclusive insights into the Federal Trade Commission’s interim reports and the future of its investigation

The evolving role of independent PBMs and their market positioning

How health-system-owned PBMs are changing the game

Fresh data on plan sponsors’ perspectives on their PBM partners

Key takeaways from PBMs’ 2025 commercial formularies

The latest shifts in PBM compensation models

The risks and rewards of PBM-affiliated private-label products and GPOs

Legislative and business implications of the 340B Drug Pricing Program

State and federal PBM regulations: What’s ahead?

Emerging controversies, challenges, and threats to watch in the industry

And much more!

As always, Dr. Fein will clearly distinguish his opinions and interpretations from the objective facts and data.

This 90-minute video webinar will feature a dedicated Q&A session, where attendees can unmute and engage directly with Dr. Fein. Don't miss this unique opportunity to gain actionable insights and have your burning questions answered in real time!

Register now to stay informed and ahead of the curve on the PBM industry!

PRICING OPTIONS

Take advantage of this exclusive educational opportunity for just $420 per viewing device. Once you register, you'll receive a unique Zoom access link within 24 hours—making it easy to add the event to your calendar and ensure you don’t miss out.

SPECIAL DISCOUNTS FOR GROUPS!

We understand that many professionals are working remotely, so we’re offering substantial savings for multiple registrations from the same organization:

Register multiple devices for as low as $295 each—a 30% discount!

Unlimited attendees can watch together at a single physical location (one registered device required).

Please contact Paula Fein (paula@drugchannels.net) to register a group for one fixed price.

Important Reminder: Each device at a single physical location must have its own registration. The webinar may not be recorded, streamed, or shared across different locations, devices, or sites.

Click here to order. All discounts will be automatically computed based on the number of registrations you enter in your cart. (You can reset the cart by entering 0 in the quantity field.)

Watch and listen via any device with a web browser (computer, iPad, iPhone/Android, etc.) There is no access via telephone.

We will use Zoom technology for this webinar. Every registrant will receive an email from Zoom with a link to watch the event. This link is unique to the registrant and can only be accessed once. We recommend that every registrant download the Zoom client software/app.

The day after the event, every registrant—whether they attended the live event or not—will receive an email from Zoom with information on how to access a video replay of the full event and download Dr. Fein's complete slide deck.

This event is part of The Drug Channels 2025 Video Webinar Series. If you already purchased access to the 2025 Drug Channels Video Webinar Series, then you should have received an email from Zoom with a link to access the April 4, 2025, event.

Organizations that purchased corporate access for The Drug Channels 2025 Video Webinar Series will receive a custom, branded signup link so employees can easily register. We will automatically refund payments from anyone at a company with corporate access who purchases a single registration using their corporate email account.

Each registration for a DCI webinar is valid for a single device at a single physical location. Each device at a physical location requires its own registration. Attendees are not permitted to record, stream, share, or project a DCI webinar to other sites or locations. Purchasers who violate this limitation by recording, streaming, sharing, or projecting a DCI webinar to other sites, devices, or locations will be liable for the full cost of all locations that viewed the webinar. DCI reserves the right to prohibit purchasers who violate our terms from attending future DCI webinars.

Today’s guest post comes from Scott Genone, Chief Product Officer at CareMetx.

Scott shares key findings from CareMetx’s recent survey of over 100 industry leaders. He explains how such advanced technologies as AI and machine learning will reshape patient services and improve the experience for both patients and healthcare providers.

On March 18, 2025, Drug Channels Institute will release The 2025 Economic Report on U.S. Pharmacies and Pharmacy Benefit Managers. This report—our sixteenth edition—remains the most comprehensive, fact-based tool for understanding the entire U.S. drug pricing, reimbursement, and dispensing system. This unique, encyclopedic resource is your ultimate guide to the complex web of interactions within U.S. prescription drug channels.

12 chapters, 500+ pages, 268 exhibits, nearly 1,200 endnotes: There is nothing else available that comes close to this valuable resource.

We are providing you with the opportunity to preorder this thoroughly updated, revised, and expanded 2025 edition at special discounted prices. This means that you can be among the first to access our new report. Those who preorder will receive a download link before March 18.

Winter—or at least February—is almost over. Celebrate the imminent return of spring with our selection of noteworthy news from around the drug channel. In this issue:

How Part D plan sponsors responded to pharmacy DIR changes

Troubling new data on copay accumulators in marketplace plans

DCI’s latest vertical integration visualization

How the IRA will hurt physician practices

Plus, cartoon cats explain the 340B Drug Pricing Program.

Today's guest post comes from Thomas Luby, Sr. Vice President, Business Development at PHIL.

Thomas discusses the challenges brands face as they manage gross-to-net (GTN) performance while simultaneously enhancing patient access and adherence. He lists the key performance indicators that can help brands improve GTN.

Abracadabra! Small pharmacies have ghosted Medicare Part D’s preferred networks—no farewell party, no breakup text, just a quiet exit.

A few months ago , DCI highlighted how the largest pharmacy chains are participating as preferred cost sharing pharmacies in the 2025 stand-alone prescription drug plan (PDP) networks. Today, we update our exclusive analysis of how smaller pharmacies are participating via their pharmacy services administrative organizations (PSAOs).

As you will see below, the largest PSAOs have almost fully abandoned PDPs’ preferred networks in 2025. Plans from Humana, WellCare, and UnitedHealthcare will again not have any independent pharmacies participating via PSAOs as preferred pharmacies.

Thanks to the Inflation Reduction Act (IRA), the PDP market is vanishing. Looks like the presence of smaller pharmacies in preferred networks will not be far behind.

This week, I’m rerunning some popular posts while I prepare for today’s live video webinar:

This week, I’m rerunning some popular posts while I prepare for today’s live video webinar:

This week, I’m rerunning some popular posts while I prepare for tomorrow’s live video webinar:

This week, I’m rerunning some popular posts while I prepare for tomorrow’s live video webinar:

This week, I’m rerunning some popular posts while I prepare for Friday’s live video webinar:

This week, I’m rerunning some popular posts while I prepare for Friday’s live video webinar:

This week, I’m rerunning some popular posts while I prepare for Friday’s live video webinar:

This week, I’m rerunning some popular posts while I prepare for Friday’s live video webinar: