Drug Channels delivers timely analysis and provocative opinions from Adam J. Fein, Ph.D., the country's foremost expert on pharmaceutical economics and the drug distribution system. Drug Channels reaches an engaged, loyal and growing audience of more than 100,000 subscribers and followers. Learn more...

Thank you, dear readers, for welcoming me into your inboxes and browsers each week. I’ve had a blast writing Drug Channels and hope that you had fun reading it.

Wishing you and your family health and happiness,

Adam

Ring in 2023 with our final news roundup of the year:

A vertical integration update

Walgreens backs away from prescriptions

Meet a cash-pay pharmacy that’s not owned by a billionaire

Time to cure or kill 340B?

Plus, Dr. Glaucomflecken helps you celebrate “I met my deductible” season!

As healthcare stakeholders continue to prioritize the move to value-based care and aim to provide equitable access to care for all, leaders must develop novel approaches to empower the patient and ensure effective risk-sharing strategies.

The Value-Based Care Summit, produced by The Healthcare Innovation Company (thINc), brings together stakeholders across all healthcare sectors, including payers, providers, and manufacturers to discuss novel approaches, innovative models, and mutually beneficial partnerships to accelerate the journey to value-based care.

Can't miss content highlights including:

Risk-Sharing and Value-Based Contracting: Examine outcomes-based strategies and innovation in payment arrangements tailored to health plan, provider, and pharma strategies

Policy and Regulations: Understand key updates from CMMI, ICER, and policy experts on value-based payment models

Value-Based Digital Solutions: Explore case studies on how to test, design, and scale digital services and ensure technological innovations

Cross-Stakeholder Partnerships: Foster collaborations to provide patient support, improve health outcomes, and lower total cost of care

Population Health and Value-Based Care: Leverage real world data and understand social determinants of health to build predictive value-based care solutions for populations

Care Delivery Transformation: Explore remote care solutions and understand patient needs to implement a value-based care delivery model

Data and Evidence: Explore data sharing, integration, and infrastructure best practices to support risk-sharing agreements and support data-driven healthcare

Two Dedicated Tracks for Your Focus Area:

For Payers & Providers

For Pharmaceutical, Biotech, and Other Manufacturers

*All registrations subject to review by the thINc team. Cannot be combined with other offers, promotions or applied to an existing registration. Other restrictions may apply.

The content of Sponsored Posts does not necessarily reflect the views of Pembroke Consulting, Inc., Drug Channels, or any of its employees. To find out how you can promote an event on Drug Channels, please contact Paula Fein(paula@drugchannels.net).

This week, I’m rerunning some popular posts while I prepare for today’s live video webinar: Drug Channels Outlook 2023.

ICYMI, the Health Resources and Services Administration (HRSA) finally got tired of my Freedom of Information Act (FOIA) requests. Shortly after I published the article below, HRSA posted public data about 340B covered entity purchases on its website. Alas, HRSA neglected to post any historical data. Fortunately, my 2022 FOIA efforts (described below) extracted purchases by 340B covered entity type for 2015 through 2021.

Here’s a summer surprise for fans of the 340B Drug Pricing Program: Drug Channels has just obtained the 2021 figures from the Health Resources and Services Administration (HRSA)! Even better, my Freedom of Information Act (FOIA) request was able to pry out detailed purchases by covered entity type.

The data tell a familiar story. For 2021, discounted purchases under the 340B program reached a record $43.9 billion—an astonishing $5.9 billion (+15.6%) higher than its 2020 counterpart. Hospitals accounted for 87% of these skyrocketing 340B purchases.

What’s more, the difference between list prices and discounted 340B purchases also grew, to $49.7 billion (+$7.0 billion). This figure approximates the money collected by 340B covered entities.

340B advocates have been screaming that “drug companies are cutting 340B,” but the data tell a very different story. Only in the U.S. healthcare system can billions more in payments and spreads be considered a cut.

Read on for full details and analysis, including the opportunity to download your very own copy of the raw data from HRSA.

Last month, IQVIA quietly released a fascinating new report on discount cards. (Link below.) The research was sponsored by the Association for Accessible Medicines (AAM).

Below, I highlight three unexpected findings from the data regarding GoodRx’s market position, when people use discount cards, how much they save, and why PBMs should still be worried about this market.

There’s a lot to unpack about the growing discount card market. As you’ll see, this report provides valuable insights about a market that seems stacked against patients.

Watch out! Plan sponsors are getting even bolder in their attempts to grab financial support intended for patients. The latest scam is called a specialty carve-out.

Here’s the game: A commercial plan eliminates coverage for all specialty drugs. Beneficiaries are then shunted over to a charitable foundation, because they are now disguised as uninsured—at least for specialty drugs. Naturally, the vendor skims a healthy share of the charity’s money.

In addition to the ethical and compliance issues, some vendors raise safety risks by sourcing prescriptions from non-U.S. pharmacies as a backup.

The Orwellian euphemism for this “benefit” design: alternative funding program.

A new survey reveals that an astounding four out of 10 commercial plans are already using, or exploring the use of, these specialty carve-out programs. Yikes.

Read on for an overview of these shady programs—and the many problems they are creating.

This makes it a good time to review the murky, little-seen economics of how commercial plan sponsors and payers access the billions of dollars in manufacturer rebates and fee that are negotiated by their pharmacy benefit managers (PBMs).

Our analyses of new Texas-mandated PBM disclosures reveal that plan sponsors receive most of the rebates, fees, and other payments from manufacturers. However, PBMs retain an unexpectedly large share of these payments—while the patients whose prescriptions generated these funds get almost nothing.

In other words, plans spread around manufacturers’ rebates and fees to offset premiums for all beneficiaries, rather than lower out-of-pocket costs for drugs that plans buy at a discounted price. Perhaps Congress will someday get around to corralling these funds.

By now, you have already read innumerable articles explaining what’s in the new Inflation Reduction Act of 2022 (IRA; P.L. 117-169).

Today, I want to highlight three significant—and presumably unintended—drug channel consequences from the hastily-passed IRA legislation. These include disruption to the now-booming biosimilar market, the prospects of physician/hospital vertical integration that will raise commercial healthcare costs and expand 340B, and the need for complex new processes to administer the IRA's lower pharmacy reimbursements.

I can only barely scratch the surface in this article, so feel free to share your own thoughts in the comments below or on social media.

At this point in our country’s history, you might think Congress would have learned the immutable law of 730-page bills: Legislate in haste, repent at leisure.

Today’s guest post comes from Leslie Small, Managing Editor, and Jinghong Chen, Reporter, at Health Plan Weekly, published by AIS Health, the journalism division of Managed Markets Insight & Technology, LLC. (MMIT).

Leslie and Jinghong discuss the terms of health insurance startups CEOs’ compensation packages. They explain why the reported CEO total compensation numbers are deceiving.

In yesterday’s post, I highlighted the largest pharmacy chains that will participate in the 2023 Medicare Part D prescription drug plans (PDP).

Today, I update our annual analyses of how smaller pharmacies will participate as preferred cost sharing pharmacies via the pharmacy services administrative organizations (PSAOs) that represent them in negotiations with plans.

As you will see below, the largest PSAOs will move further away from preferred networks in 2023. What's more, plans from Aetna, Humana, WellCare, and UnitedHealthcare will not have any independent pharmacies participating via PSAOs as preferred pharmacies.

Below we provide details about the PSAOs owned by the three major wholesalers—AmerisourceBergen, Cardinal Health, and McKesson—along with information about AlignRx, the largest independent PSAO. There are some differences in strategy, as you will see from our handy scorecard below. However, smaller pharmacies’ near-total rejection of preferred networks shows that the more the PBMs talk, the less independents can take.

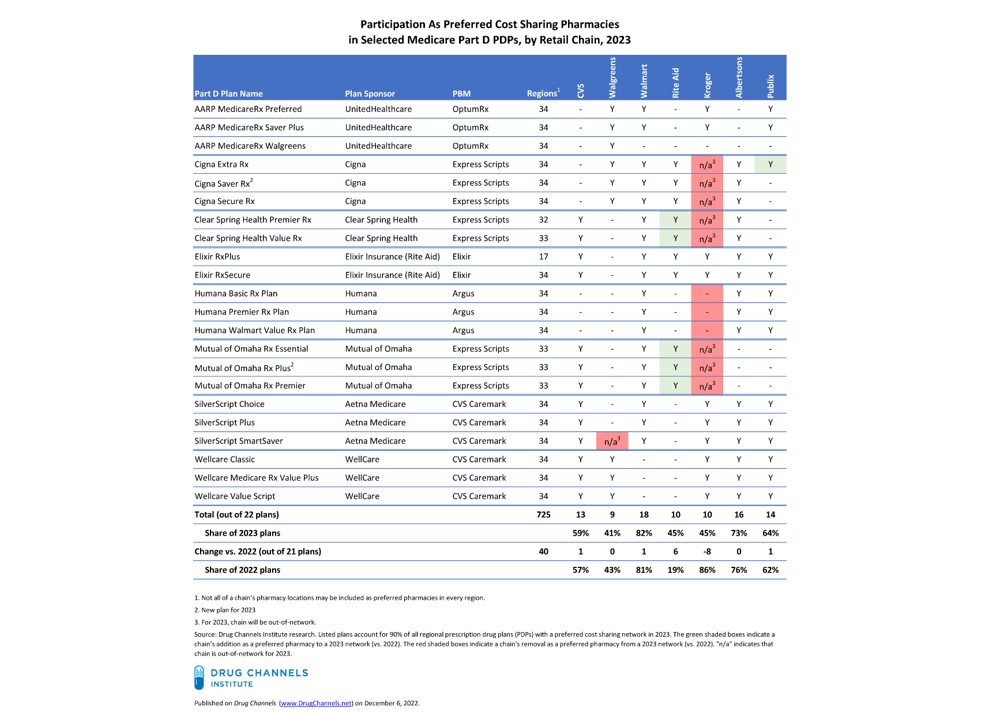

Today, I examine the seven largest retail chains’ 2023 participation in the 22 major 2023 Part D preferred networks that the eight largest plan sponsors will offer. As always, I offer you a handy table for scoring each chain’s participation and changes from 2022 to 2023.

As you’ll see, Kroger’s decision to exit Express Scripts commercial pharmacy networks has had negative ramifications for its Part D position. Kroger will be out-of-network—not just non-preferred—in the major Part D networks for which Express Scripts acts as the PBM. That will be a key factor behind its $1+ billion revenue hit.

Today’s guest post comes from Deepak Thomas, Founder and CEO of PHIL Inc.

Deepak explains how a manufacturer’s net revenues are affected when that manufacturer helps patients access, afford, and adhere to medication therapy. He provides three suggestions for building a channel strategy to optimize gross-to-net while also improving clinical, financial, and operational outcomes.

This week, I’m rerunning some popular posts while I prepare for today’s live video webinar:

This week, I’m rerunning some popular posts while I prepare for today’s live video webinar:

This week, I’m rerunning some popular posts while I prepare for tomorrow’s live video webinar:

This week, I’m rerunning some popular posts while I prepare for tomorrow’s live video webinar:

This week, I’m rerunning some popular posts while I prepare for tomorrow's live video webinar:

This week, I’m rerunning some popular posts while I prepare for tomorrow's live video webinar:

This week, I’m rerunning some popular posts while I prepare for this Friday’s live video webinar:

This week, I’m rerunning some popular posts while I prepare for this Friday’s live video webinar: