This week, I’m rerunning some popular posts while I prepare for this Friday’s live video webinar: PBM Industry Update: Trends, Controversies, and Outlook.

This week, I’m rerunning some popular posts while I prepare for this Friday’s live video webinar: PBM Industry Update: Trends, Controversies, and Outlook.Click here to see the original post and comments from January 2022.

Each exclusion list contains 400 to 500 products. Growth in the number of excluded drugs slowed, due partly to the fact that so many drugs have already been dropped from PBMs’ formularies.

Below, I highlight five observations about this year’s lists, including unexplainable differences in how PBMs handle specialty drugs, biosimilars, and insulin.

I also offer some thoughts on non-medical switching and what we still don’t know about how exclusions affect patients.

Let me know what you think by commenting below or on social media.

UNPICK ME

Formulary exclusions have emerged as a powerful tool for PBMs to gain additional negotiating leverage against manufacturers. The prospect of exclusion leads manufacturers to offer deeper rebates to avoid being cut from the formulary. Exclusions are one of the key factors behind the large gap between list and net prices for brand-name drugs. (See Tales of the Unsurprised: Brand-Name Drug Prices Fell for the Fourth Consecutive Year.) They can also affect a patient’s out-of-pocket costs and access to a particular therapy.

Formulary exclusions block access to specific products on a PBM’s recommended national formulary. These are suggestions, not mandates. Thus, a drug’s appearance on an exclusion list does not guarantee that all patients will lose access. Plan sponsors—the PBM's clients—can choose not to adopt their PBM’s standard formulary. However, they would then face reduced rebates and/or higher plan costs.

Here are the 2022 formulary updates for commercial clients of the three largest PBMs:

- CVS Caremark: 2021 Standard Control Formulary Removals and Updates and Advanced Control Specialty Formulary

- Express Scripts: 2022 National Preferred Formulary Exclusion (12/10/21)

- OptumRx: 2022 Premium Standard Formulary

PBMs now target both traditional and specialty products for formulary exclusion. The excluded products typically fall into one or more of the following categories:

- Brand-name products with generic equivalents or therapeutic alternatives

- Biosimilars and reference biologics with biosimilar alternatives

- Non-preferred (tier 3) drugs with very low utilization

- Heavily promoted drugs in therapeutic classes with multiple generic alternatives

- Medicines treating chronic conditions

You can read our review of the 2021 lists here: The Big Three PBMs Ramp Up Specialty Drug Exclusions for 2021.

WELCOME TO 2022

Here are five takeaways from the 2022 exclusions.

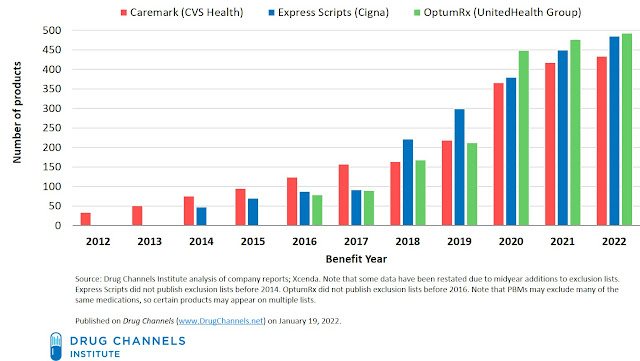

1. Exclusions continue to grow, albeit more slowly.

The practice of formulary exclusion began in 2014. Since then, the number of unique products excluded from the formularies of the three largest PBMs—Caremark (CVS Health), Express Scripts (Cigna), and OptumRx (UnitedHealth Group)—has grown dramatically.

The chart below tracks the growth at each company. As you can see, the rate of growth has slowed somewhat, due partly to the large number of products that have already been dropped.

We counted the number of unique products on each company’s 2022 list. Here’s what we found:

The chart below tracks the growth at each company. As you can see, the rate of growth has slowed somewhat, due partly to the large number of products that have already been dropped.

[Click to Enlarge]

We counted the number of unique products on each company’s 2022 list. Here’s what we found:

- For 2022, CVS removed 20 drugs and added four drugs back, increasing its list to an estimated 433 products.

- Express Scripts expanded its exclusion list to an estimated 485 products.

- OptumRx increased its exclusion list to an estimated 492 products.

2. Specialty exclusions are now routine.

As we predicted last year, PBMs’ formulary exclusions have become common for the previously untouchable specialty drug categories. This growth in excluded specialty products shows how competitive many specialty therapy categories have become.

Express Scripts and CVS Caremark use an indication-specific formulary for the inflammatory conditions drug class. They each list preferred and excluded options by condition. Consider the ulcerative colitis indication. At Express Scripts, Simponi and Xeljanz are preferred after patients step through Humira. At CVS Caremark, Stelara, Xeljanz, and Zeposia (a 2022 addition) are preferred only after patients step through Humira. By contrast, OptumRx’s formulary doesn’t distinguish products and conditions.

Humira’s position as first-line treatment reflects both AbbVie’s formulary negotiations as well as the PBMs’ positioning for 2023. That’s when Humira will face at least seven biosimilar competitors—some of which will be interchangeable with Humira.

In the Drug Channels October news roundup, I highlighted a fantastic IQVIA report on PBM formulary exclusions for oncology drugs. This report documented soaring exclusions—even for oncolytics that lack a generic or biosimilar alternative. My examination of the PBMs’ 2022 lists finds exclusions of many single-source, brand-name oncology products.

The exclusions of non-biological specialty drugs with generic equivalents are not generally controversial. Last year, Express Scripts excluded Tecfidera, which now has an approved generic. For 2022, both CVS and OptumRx will also exclude the brand-name version. Alas, the warped incentives baked in Part D plans have led to formularies that prefer the brand name over the generic, as 46Brooklyn explains in Wreck-fidera: How Medicare Part D has hidden the benefits of generic competition for a blockbuster Multiple Sclerosis treatment.

Express Scripts and CVS Caremark use an indication-specific formulary for the inflammatory conditions drug class. They each list preferred and excluded options by condition. Consider the ulcerative colitis indication. At Express Scripts, Simponi and Xeljanz are preferred after patients step through Humira. At CVS Caremark, Stelara, Xeljanz, and Zeposia (a 2022 addition) are preferred only after patients step through Humira. By contrast, OptumRx’s formulary doesn’t distinguish products and conditions.

Humira’s position as first-line treatment reflects both AbbVie’s formulary negotiations as well as the PBMs’ positioning for 2023. That’s when Humira will face at least seven biosimilar competitors—some of which will be interchangeable with Humira.

In the Drug Channels October news roundup, I highlighted a fantastic IQVIA report on PBM formulary exclusions for oncology drugs. This report documented soaring exclusions—even for oncolytics that lack a generic or biosimilar alternative. My examination of the PBMs’ 2022 lists finds exclusions of many single-source, brand-name oncology products.

The exclusions of non-biological specialty drugs with generic equivalents are not generally controversial. Last year, Express Scripts excluded Tecfidera, which now has an approved generic. For 2022, both CVS and OptumRx will also exclude the brand-name version. Alas, the warped incentives baked in Part D plans have led to formularies that prefer the brand name over the generic, as 46Brooklyn explains in Wreck-fidera: How Medicare Part D has hidden the benefits of generic competition for a blockbuster Multiple Sclerosis treatment.

3. Insulin exclusions remain mystifying.

Exclusions are a key factor driving gross-to-net differences for insulin products. Nearly one in five formulary exclusions from 2014 to 2020 was for diabetes treatments. (source) For example, Express Scripts and OptumRx are aligned with Eli Lilly’s Humalog and Humulin, but exclude Novo Nordisk’s NovoLog and Novolin. By contrast, CVS Health’s formulary excludes Lilly’s insulins in favor of Novo Nordisk’s products.

However, the launch of the first interchangeable biosimilar insulin has led to some truly bonkers formulary decisions. For background, see Why PBMs and Payers Are Embracing Insulin Biosimilars with Higher Prices—And What That Means for Humira.

As I describe in that article, Viatris has launched two identical versions of its interchangeable biosimilar for Lantus, a long-acting insulin:

However, the launch of the first interchangeable biosimilar insulin has led to some truly bonkers formulary decisions. For background, see Why PBMs and Payers Are Embracing Insulin Biosimilars with Higher Prices—And What That Means for Humira.

As I describe in that article, Viatris has launched two identical versions of its interchangeable biosimilar for Lantus, a long-acting insulin:

- Semglee (insulin glargine-yfgn) injection, a branded interchangeable product with a high list price

- Insulin Glargine (insulin glargine-yfgn) injection, an unbranded, authorized interchangeable biosimilar with a low list price

- CVS Caremark prefers Basaglar, a non-interchangeable follow-on biologic, and blocks Lantus. Neither Semglee nor its unbranded version is listed on the Caremark formulary.

- Express Scripts prefers the high-list price Semglee and excludes the low-priced, unbranded interchangeable biosimilar. (The unbranded version is preferred on the PBM’s little-used Flex formulary.)

- OptumRx prefers the Lantus reference product and excludes Semglee. However, its formulary list doesn’t mention the unbranded biosimilar.

4. Biosimilar exclusions are also baffling.

PBMs continue to juggle provider-administered biosimilars on their pharmacy benefit formularies. Consequently, plans do not consistently favor biosimilars and continue to restrict providers’ clinical choices.

Consider Remicade and its biosimilars. For 2022, the Express Scripts NPF prefers the Inflectra biosimilar, and excludes Remicade and two of its biosimilars: Avsola and Renflexis. OptumRx prefers Avsola and Inflectra, but excludes Remicade and Renflexis. Meanwhile, CVS Caremark prefers Remicade and excludes all three biosimilars.

Huh?

What’s more, Express Scripts’ exclusion of Avsola is especially ironic. Last July, Cigna, the parent company of Express Scripts, shifted Avsola and Inflectra to preferred status on its formulary. It also offered patients a $500 debit card to switch to one of these biosimilars. What happened to the patients who took Cigna’s offer an switched to Avsola?

There are similarly puzzling decisions for the biosimilars of such oncology reference products as Avastin, Herceptin, Neulasta, and Rituxan. These formulary strategies slow biosimilar adoption by raising costs for providers and wholesalers. (See Section 6.4.3. of our 2021-22 Economic Report on Pharmaceutical Wholesalers and Specialty Distributors.)

Note that these products are typically reimbursed under the medical (not pharmacy) benefit, so PBMs play a limited role in managing these categories. However, the growth of white bagging has increased the importance of PBM formularies—and PBMs’ specialty pharmacies—for provider-administered drugs. See White Bagging Update: PBMs’ Specialty Pharmacies Keep Gaining on Buy-and-Bill Oncology Channels.

Consider Remicade and its biosimilars. For 2022, the Express Scripts NPF prefers the Inflectra biosimilar, and excludes Remicade and two of its biosimilars: Avsola and Renflexis. OptumRx prefers Avsola and Inflectra, but excludes Remicade and Renflexis. Meanwhile, CVS Caremark prefers Remicade and excludes all three biosimilars.

Huh?

What’s more, Express Scripts’ exclusion of Avsola is especially ironic. Last July, Cigna, the parent company of Express Scripts, shifted Avsola and Inflectra to preferred status on its formulary. It also offered patients a $500 debit card to switch to one of these biosimilars. What happened to the patients who took Cigna’s offer an switched to Avsola?

There are similarly puzzling decisions for the biosimilars of such oncology reference products as Avastin, Herceptin, Neulasta, and Rituxan. These formulary strategies slow biosimilar adoption by raising costs for providers and wholesalers. (See Section 6.4.3. of our 2021-22 Economic Report on Pharmaceutical Wholesalers and Specialty Distributors.)

Note that these products are typically reimbursed under the medical (not pharmacy) benefit, so PBMs play a limited role in managing these categories. However, the growth of white bagging has increased the importance of PBM formularies—and PBMs’ specialty pharmacies—for provider-administered drugs. See White Bagging Update: PBMs’ Specialty Pharmacies Keep Gaining on Buy-and-Bill Oncology Channels.

5. Patients and their physicians continue to get bounced around.

Those in the market access game understand that exclusions reflect negotiations between pharmaceutical manufacturers and PBMs. As they say: It’s not personal. It’s strictly business.

But for patients and physicians, these formularies can have important real-world consequences.

An individual patient’s access to a particular therapy and out-of-pocket costs are determined by formulary exclusions established by their plan’s PBM. What’s more, some products are covered by one or two of the PBMs, but excluded by the others. Patients who change plans (or employers) can unknowingly lose access to their physician’s preferred therapy—unless they file a successful appeal, i.e., scale the paperwork mountain.

Exclusions also raise the prospect of non-medical switching—altering a patient’s drug therapy for reasons other than a drug’s efficacy, side effects, or clinical outcome.

Consider the direct oral anticoagulant (DOAC) category. For 2022, CVS Caremark began excluding Bristol-Myers Squibb’s Eliquis in favor of Janssen’s Xarelto. (It continues to exclude Pradaxa.) Meanwhile, OptumRx places all three products on its second formulary tier. Express Scripts prefers Eliquis and Xarelto, but excludes Pradaxa.

Fourteen patient groups have urged CVS Caremark to reverse its exclusion, writing: “This abrupt change will be dangerously disruptive for patients currently on therapy and reliant upon a previously covered DOAC to manage their cardiovascular risk.”

How many physicians know which of their patients are covered by each PBM? And how many want to change a patient’s treatment strategies for this category based on this year’s formulary exclusion or a patient’s change of insurance?

These issues are not new. If you missed it last year, I recommend reading physicians’ comments—and the rebuttal from Express Scripts—in this 2020 Healio Rheumatology article: Formulary exclusions, non-medical switching jeopardize disease control, patient trust.

But for patients and physicians, these formularies can have important real-world consequences.

An individual patient’s access to a particular therapy and out-of-pocket costs are determined by formulary exclusions established by their plan’s PBM. What’s more, some products are covered by one or two of the PBMs, but excluded by the others. Patients who change plans (or employers) can unknowingly lose access to their physician’s preferred therapy—unless they file a successful appeal, i.e., scale the paperwork mountain.

Exclusions also raise the prospect of non-medical switching—altering a patient’s drug therapy for reasons other than a drug’s efficacy, side effects, or clinical outcome.

Consider the direct oral anticoagulant (DOAC) category. For 2022, CVS Caremark began excluding Bristol-Myers Squibb’s Eliquis in favor of Janssen’s Xarelto. (It continues to exclude Pradaxa.) Meanwhile, OptumRx places all three products on its second formulary tier. Express Scripts prefers Eliquis and Xarelto, but excludes Pradaxa.

Fourteen patient groups have urged CVS Caremark to reverse its exclusion, writing: “This abrupt change will be dangerously disruptive for patients currently on therapy and reliant upon a previously covered DOAC to manage their cardiovascular risk.”

How many physicians know which of their patients are covered by each PBM? And how many want to change a patient’s treatment strategies for this category based on this year’s formulary exclusion or a patient’s change of insurance?

These issues are not new. If you missed it last year, I recommend reading physicians’ comments—and the rebuttal from Express Scripts—in this 2020 Healio Rheumatology article: Formulary exclusions, non-medical switching jeopardize disease control, patient trust.

UNDERSTANDING THE PATIENT IMPACT

The ever-growing presence of exclusions—and differences between PBMs’ lists—raises important issues about patient care.

CVS has stated that only 0.4% of its members will be affected by its 2022 exclusions, which is comparable to the 2021 figure. Express Scripts has stated that only 0.3% of its members will be affected by the 2022 exclusions. That’s down from the 1.3% of beneficiaries who were affected by its 2021 exclusions.

These figures may seem low, but they are more significant than they appear. Specialty drugs are utilized by a small share of the population, so the growth of exclusions for these products could affect these patients disproportionately.

IMHO, PBMs should provide more transparency into how formulary changes affect patients taking drugs for cancer and for other specialty therapies. There is also an urgent need for more research on how exclusions affect physicians’ prescribing decisions, patients’ ability to access therapies, and clinical outcomes.

What are your thoughts?

No comments:

Post a Comment